zonination / investing

- четверг, 30 июня 2016 г. в 03:12:59

R

Investing Returns on the Market as a Whole

Source file stocks.csv last updated on 2016-06-24.

Note that this stock market simulation assumes a portfolio that is invested in 100% US Stocks. While a lot of the results show that 100% Stocks can generate an impressive return, this is not an ideal portfolio.

A portfolio should be diversified with a good mix of US Stocks, International Stocks, and Bonds. This diversification helps to hedge against market swings, and will help the investor to optimize returns on their investment with lower risk than this visual demonstrates.

In addition to this, this curve only looks at one lump sum of initial investing. A typical investor will not have the capital to employ a single lump sum as a basis for a long-term investment, and will instead rely on dollar cost averaging, where cash is deposited across multiple years (which helps to smooth out the curve as well).

If you are interested in reviewing your asset allocation or auditing your portfolio, check out the Further Reading section below.

A lot of you know me from my comments and posts on Reddit's /r/personalfinance. I have also recently been spending a lot of time at /r/dataisbeautiful as well. This started off as my first dataviz project a while back. I downloaded some data based on Robert Shiller's work and went crazy with it. Now that I've finally settled in and gotten other projects completed, I picked this one back up and decided to finally drive it to completion.

"Warren [Buffet], it strikes me that if you did nothing else you never sell. That is, if you can grit your teeth through and just disregard short-term declines in the market or even long-term declines in the market, you will come out well. I mean you just stick all your money in stocks and go home and don’t look at your portfolio you’ll do far better than if you try to trade it." - Alan Greenspan

A lot of people on /r/personalfinance, usually green to the wonders of long-term investing, often question the security of the "buy and hold" strategy, or would rather try to time the market instead. This viz project is an attempt to do three things:

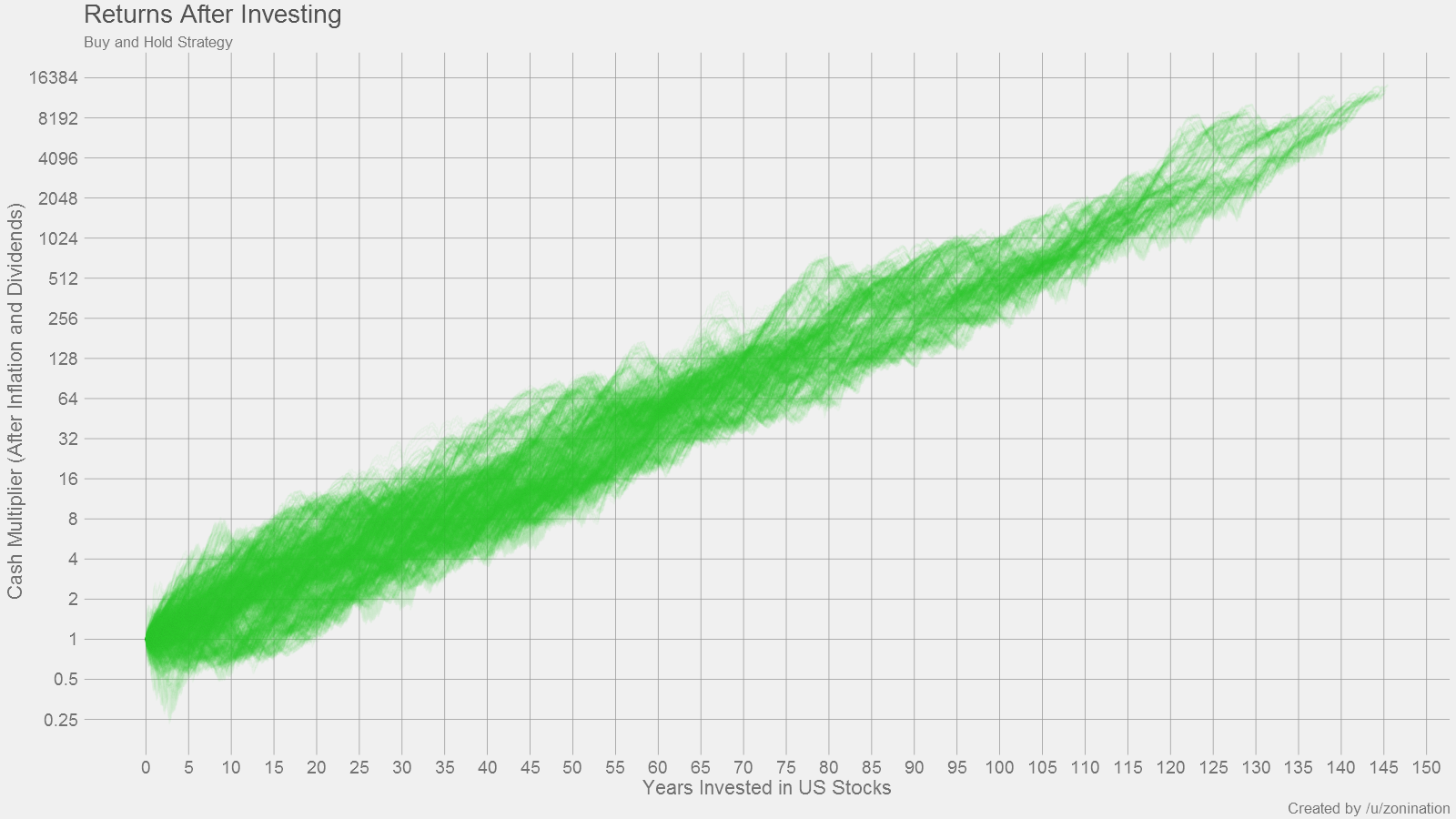

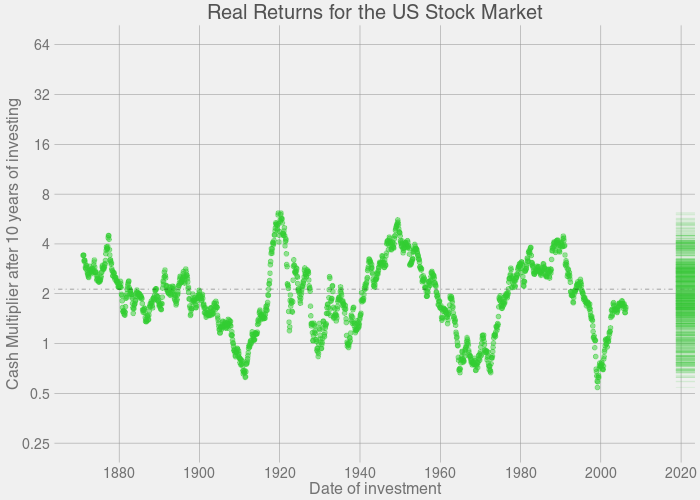

Final Plot:

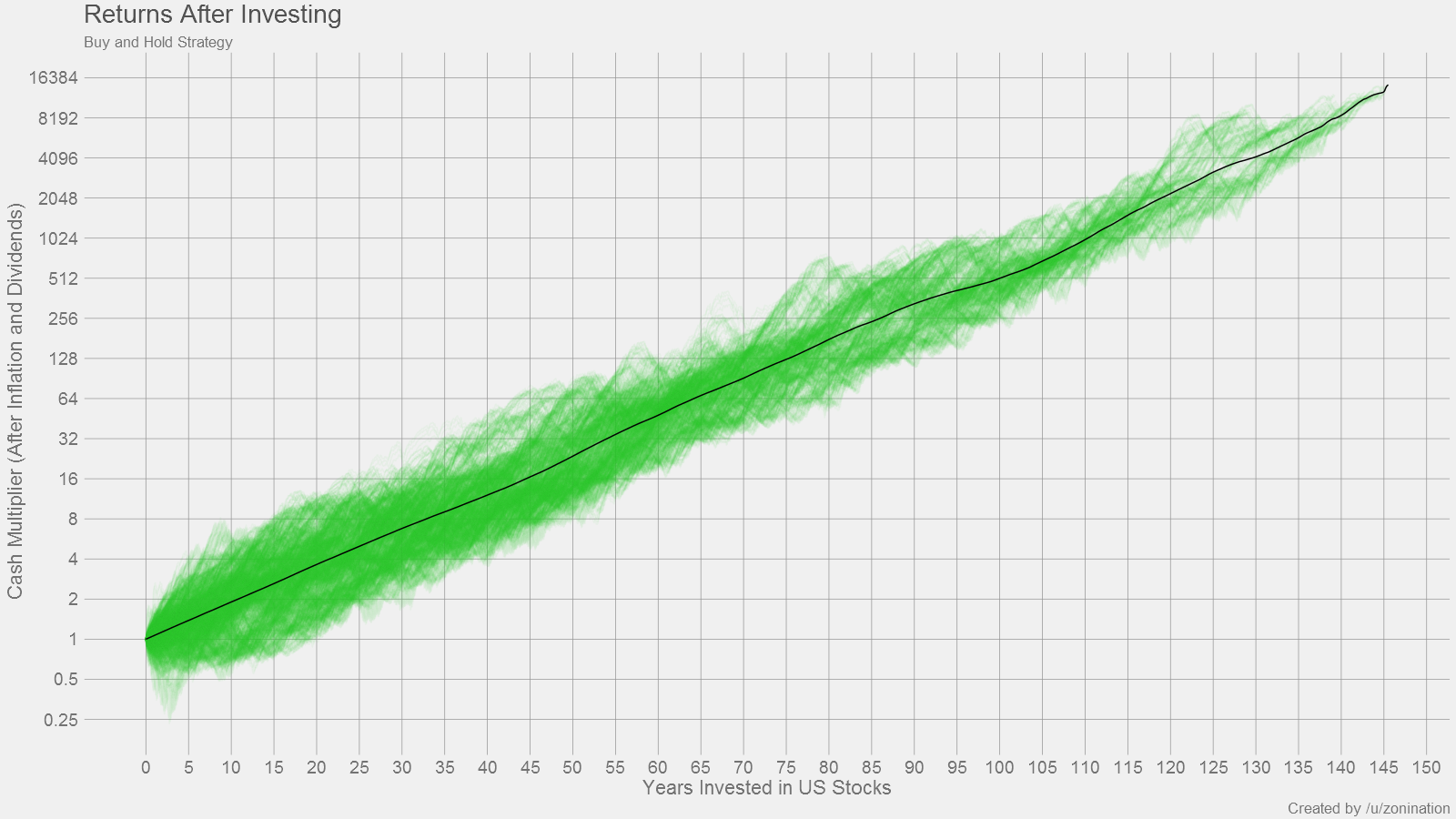

Final Plot with Average markings:

The plots above were generated based on past returns in the S&P500. So at Year 1, we take every point on the S&P500 curve, look at every point on the S&P500 that's one year ahead, add in dividends and subtract inflation, and record all points as a relative gain or loss for Year 1. Then we do the same thing for Year 2. Then Year 3. And so on, ad nauseum. The program took a couple hours to finish crunching all the numbers.

In short, for the plots above: If you invest for X years, you have a distribution of Y possible returns, based on previous history.

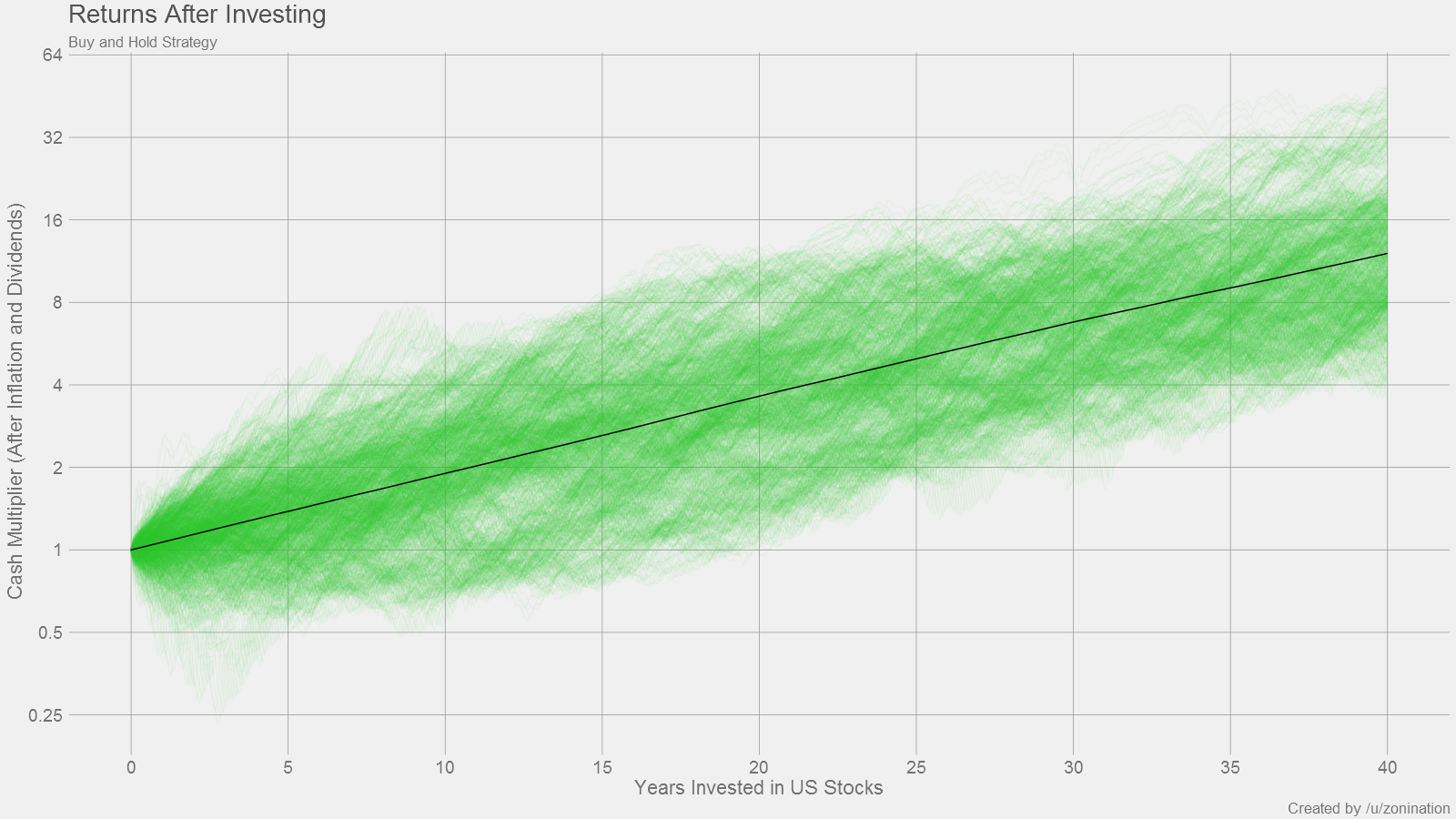

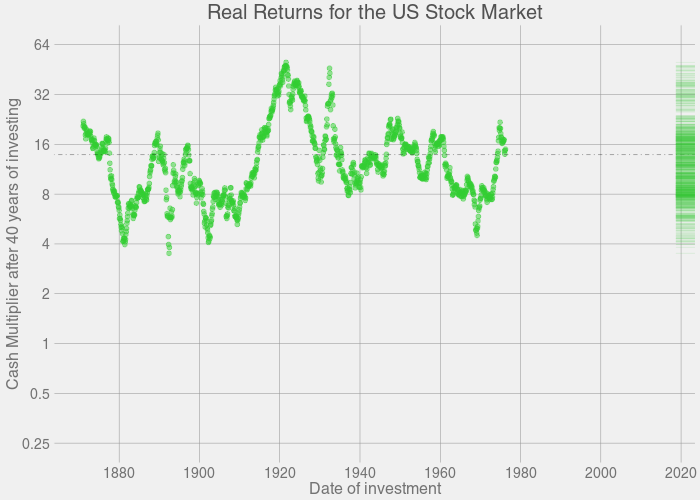

I can already hear the keyboards being tapped for the comments section: "Wait, Zoni! this is over the span of 145 years! Nobody is ever going to live to invest for that long." I know, so let's take a look at a more realistic span of investing. Let's say you start investing at the age of 20, and then retire at age 60, which gives you 40 years of investing. So after a quick subset(stocks,year<=40). Here's what that snapshot will look like:

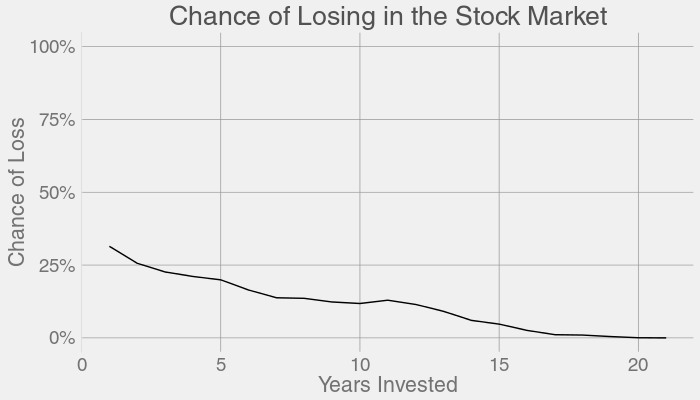

Wait a minute. Zoom in. What's going on with those data points that are losing money over X years?

Keep in mind that this is a distribution of returns. After 1 year of investing, you might sell high or you might sell low. After 20 years, you're almost guaranteed to sell high. By 40 years, you're turning a major profit. So now what's our probability of losing cash for each possible year of investing? Code provided here

Some of the worst market downturns are also represented here, like the Great Depression, the 1970s recession, Black Monday, the Dot-Com Bubble, the 2008 Financial Crisis. But note how they completely recover to turn a profit after some more time in the market.

Here's the list of years you can invest, and still be down. Take note that some of these years cover the same eras:

(code :unique(subset(stocks,multip<1&year==20)$inv.year))

But that doesn't consider all the years that were average, or even the years that were extremely profitable for investors. Here's the same plot above, except with a 0% to 100% scale for better perspective:

Long story short, buy and hold. Invest for the long-term, and not the short-term. Don't try to time the market; even if you invested at market peaks, you'd still make out well.

What about Dollar Cost Averaging (DCA) instead of Lump Sum Investing (LSI)?

This one is going to be a little more difficult. I've included the original code and it's open-source, so if you want to play with the numbers, you can try to do this yourself. However, there are a couple points I'd like to keep in mind:

My prediction is that DCA will "thin out" the plot and bring a lot more values closer to the average. This makes investing a bit safer, but at the cost of slower gains.

This portfolio is 100% stocks. What about Bonds? International Stocks? How about a three-fund portfolio?

Working with this kind of data would be my wet dream. If anyone has data on International Stocks, Bonds, Bills, Cash, Bitcoin, or other values you want similar plots of, in a similar format to the SP500 data, please send me a PM on Reddit.

One day, I hope to simulate a three-fund portfolio.

What if the market crashes right before retirement and the world ends up broke and the dollar crashes?

Okay, a few notes here:

This viz actually started off as an animation. Below is the original plot for the animation:

I'll step through a few freeze-frames of the plot above:

The code for these plots is shared in the altplots folder.